Skip to content

Data Science @ Statnett

Home

Contact

About us

Search

Uncategorized

May 7, 2018

Comparing javascript libraries for plotting

Thomas Trötscher

April 27, 2018

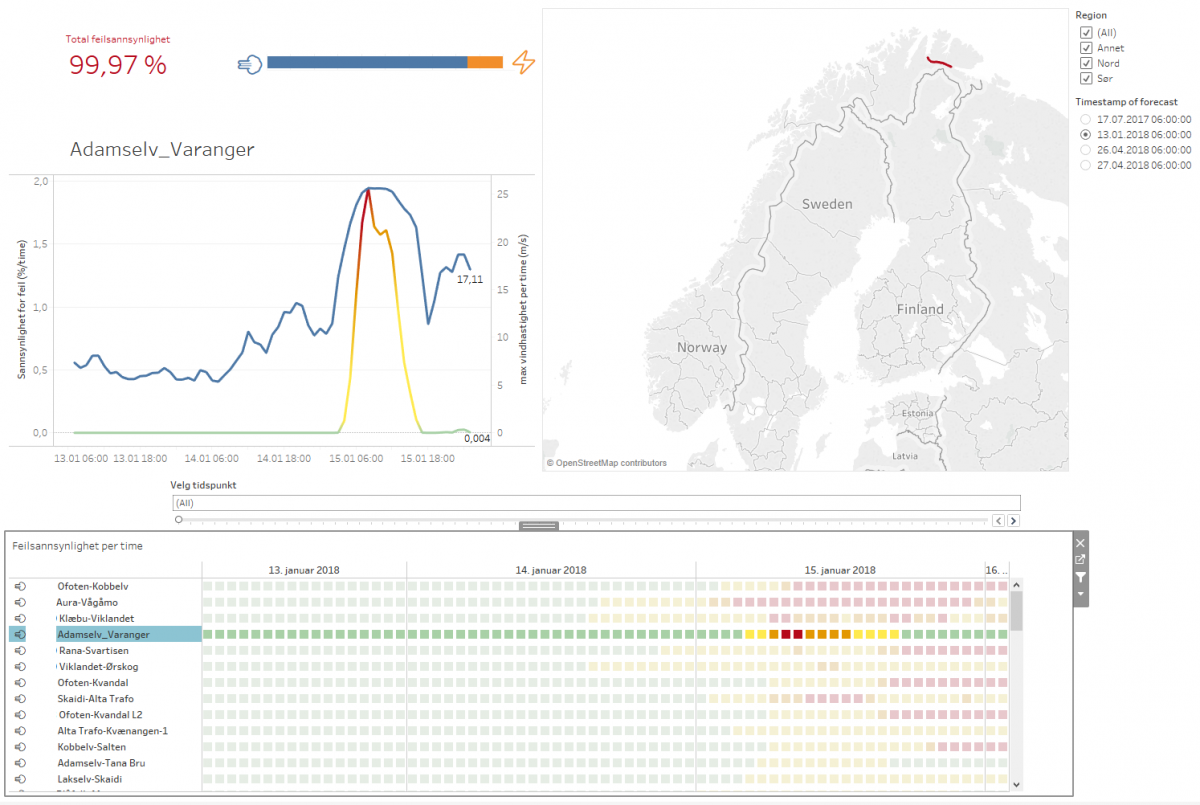

Setting up a forecast service for weather dependent failures on power lines in one week and ten minutes

Gerben Dekker

April 23, 2018

Estimating the probability of failure for overhead lines

Thomas Trötscher

Previous Page

1

2

Loading Comments...

Write a Comment...

Email (Required)

Name (Required)

Website